The sails are torn and fluttering fiercely like flags in a windstorm. The ship has stopped slicing through the waves, and its timbers are shuddering on the rocks. You can hear the stony teeth chewing into her planks, but the captain and crew are passing around sherry glasses and raising a toast to the fine weather, assuring the passengers that all is well.

You can hear the tearing of financial sails everywhere in the world right now, and that includes right here on the USS Bailout where Captain Powell reaffirms that the job market is strong and the economy resilient even as we hear the hull grinding under our feet. First Mate Yellen smiles her grandma grin from the tilting crow’s nest and assures everyone below she sees no land or rocks in site.

Yet, on Friday (Sept. 30), all major US stock indices ended the quarter with a decisive thud at new lows for the year. They’ve pounded downward quarter after quarter after quarter, but “we’re not in a recession yet” is all we hear called out from the watch on deck. We are now nine full months into this stormy year, and every quarter has ended lower for all indices and for GDP, and we’re now taking on water faster than ever, but “all is well!” In fact, yesterday (Friday) delivered the S&P’s worst monthly decline since the Covid calamity of 2020.

I wrote a short article at the start of the day yesterday to sum our situation up, saying we were going “Down, Down, Down in a Burning Ring of Fire,” that fire being inflation, forcing the Fed to fight it with all it has. The Fed believes it needs to take an already crippled labor market and submerse it deeper to suppress the flames of inflation. It’s making the greatest mistake in Fed history. If you have to sink the ship to extinguish the fire, it’s not going to help. (If you want to know why, you can read all about it in an article that lays out the biggest Fed blind spot in history: “Everyone Sings the “Strong Labor Market” Tune in Unison as the Band Plays on, and They’re All DEAD Wrong!“)

We are also three full quarters into the year, and each of the first two quarters ended with GDP deeper below the waterline. The Fed’s GDPNow estimator, which looks ahead to guess where the present quarter will end, recently hit the deck where it lay at the end of the last quarter, too, and the one before that, both of which, then, sank further underwater as we got closer to the calculations of GDP actually being released. It has, however, bounced more erratically in the third quarter than I’ve ever seen, showing just how choppy the present seas have been.

Bonds behaving badly

Bond markets all over the world, including the US, are crashing harder by a number of measures than they have in forty years. The UK bond market became such a catastrophe this week, the Bank of England had to rush in with a major reversal from its plans to tighten the financial world by withdrawing quantitative sums of cash to, instead, creating quantitative sums of cash out of nothing “on whatever scale is necessary” all over again to ease the financial markets — a total reversal. We’re back to “whatever it takes,” and the BOE didn’t even get started with tightening! That’s how bad it is!

Why? Because pensions funds were self-destructing. As Zero Hedge summarized it:

Billions In Margin Calls “Death Spiraling” into a Complete Bond Market Collapse, Pension Fund Wipe Out

Noting the stem-rot in the brains of our leaders, they also commented…

It’s only fitting that literally hours after the most clueless dwarf in capital markets history, Janet “No crisis in my lifetime” Yellen said that financial markets are functioning well, that the Bank of England literally panicked, and shocked markets by resuming unlimited QE.

“We haven’t seen liquidity problems develop in markets — we’re not seeing, to the best of my knowledge, the kind of deleveraging that could signify some financial stability risks,” Yellen said in answering reporters’ questions

Then she fell out of her old crow’s nest and broke her head upon the rocks that were right beneath her … or … actually …

Then, a few hours later, the Bank of England saw liquidity problems that looked like a beach suddenly emerging as the first negative wave of a tsunami runs out, citing “significant repricing of UK and global financial assets” across the board.

According to the Financial Times the problem was,

Thousands of pension funds have faced urgent demands for additional cash from investment managers in recent days to meet margin calls, after the collapse in UK government bond prices blew a hole in strategies to protect them against inflation and interest-rate risks.

Billions of pounds in pension funds faced immediate collateral risks, forcing them to sell off various assets to raise cash to cover their bets. Those sales were crashing the value of all those other assets like a fire sale. The demand for collateral was large enough to crash the entire bond market in another twenty-four hours if the BOE didn’t step in as the new emergency buyer of first resort.

How did that come out of nowhere? Well, I’ll tell you. It didn’t. Funds, of course, were over-leveraged again because we’ve been feeding leveraged greed for years with cheap credit, and now we’re raising the cost of credit everywhere. It should be self-evident that is impossible to pull off. Whatever rises on the flood tide of QE, subsides on the ebb tide of QT. Oh, but who would have thought that greed would have caused investors to over-leverage their risks or keep them from adjusting their risks ahead of clear central-bank schedules? After all, we were assured there was no moral hazard building up from all the bailouts in the past.

But that’s how it is with these “black swans.” They are more like black sea monsters, shadows that move beneath the deep. They are often things our financial leaders and even investors could have and should have seen as reasonably high likelihoods — shadows sliding right beneath our sails — but didn’t. Suddenly, they burst as monsters out of the sea right in in front of us. Janet’s colleagues in the UK certainly should have seen the potential for this bond bust building, but they didn’t … probably because no one wanted them to. Greed is so profitable if you just let it happen. Until it isn’t. But that’s what bailouts are for.

This became the volatility shock of a generation for the bond market because, in less than twenty-four hours, the UK bond turmoil was already spreading contagion to other national markets:

Turmoil in UK government debt has sent shockwaves through global markets, sparking big swings in US and European bonds.

“Bond markets are always highly correlated, but we’ve definitely seen the tail wagging the dog this week,” said Dickie Hodges, head of unconstrained fixed income at Nomura Asset Management. “The moves in gilts were so big that they filtered through to European and US bond markets.”

The problem sprang up so quickly that one commentator exclaimed,

Had they not intervened, there would have been mass insolvencies of pension funds by THIS AFTERNOON.

Now, that’s a crisis! But, hey, everything’s steady. Just as Janet assured us. No land or rocks anywhere on the horizon. (Just under us.)

Some of the outfall resulted in a flood tide of capital to the US, helping the US out, but the effect didn’t last past a day before the tide ran the other way because of the extreme volatility in how all markets, shallow as they now are in willing traders, are breaking down so badly.

“Even though the UK is a basket case of its own making, the fact is the same pressures are being acutely felt elsewhere,” said Richard McGuire, a rates strategist at Rabobank. “Investors see the government’s ill-conceived experiment, and wonder if it’s a sign of things to come in other countries.”

Of course it is! The whole global economy is shivering throughout its timbers because they’ve all been running the same game. And, of course, what the Bank of England did was immediately bail out greed. Who pays? The little guys who are hit worse by the increase in inflation that will come with going back to money printing to save the big guys from their many over-leveraged, risky positions … and, if the bailout didn’t happen, the little guys would still pay through the loss of their pensions.

The shock waves that crossed the Atlantic like a tsunami caused Bank of America to warn at the close of the business week that the credit market has reached critical levels of stress:

With credit stress approaching critical levels, now is the time to put emphasis on risk management. This means slower pace of rate hikes at immediate upcoming meetings and a potential pause subsequently, to allow the economy to fully adjust to all the extreme tightening already implemented, but still working its way through the financial system’s plumbing. Failure to do so raises the risk of credit market dysfunction, which, if occurred, would be difficult to contain and fix.

In other words, when the waves are this high above the gunnels, let’s stop rocking the boat so hard and see how things settle for a bit. Of course, if the Fed did take a mere pause, the insane stock market would take that as a sign it was time to spike risks to the moon again with more leveraged investments because the greed has grown that stupid due to force-Fed intoxication.

Fed reckoning is dead

The Fed could heed the warning, but it won’t. It will keep its sails set tight, even stranded on the rocks with the wind pushing hard onto the rocks because it believes the tight labor market means the labor market is strong, not that it is seriously deficient in supply and, therefore, incapable of sustained production.

During all the upheaval on Friday …

Vice-Chair Brainard noted policy will need to be restrictive for some time to have the confidence in inflation moving back to the 2% target, adding she is committed to avoiding pulling back prematurely.

Yet, if the labor market is tight because the economy is strong, as the Fed claims and everyone believes along with it because, well, it’s the Fed, then why did the Chicago Purchase Managers Index plunge back into contraction for the first time since the very deep Coronacrash:

Every single component in the index fell off a cliff.

At the same time, the Fed’s most-favored inflationary gauge rose to the hottest it’s been in decades — hardly a move giving the Fed latitude to back down on its tightening as the economy crashes deeper and deeper into recession. So, with stock indices all at new lows for the year and bonds and bond funds at new lows in valuation and the Chicago PMI finally showing the economic contraction that GDP has been showing all year, but with inflation soaring higher than ever, what a blow-up the bursting of the Everything Bubble is turning out to be.

The Fed’s preferred gauge shows inflation accelerated even more than expected in August.… Headline inflation, including food and energy, also accelerated, despite a sharp drop in gasoline prices.

While CNBC went on to describe the bad metrics within the PCE inflation gauge, it never quite said outright that this was the worst inflation reading on that gauge in decades — just worse than expected. However, it was, in fact, the worst in decades:

I had to go dig up a graph from the Fed, and it shows prices have never been higher:

The gauge dipped a little in July, but then went higher by the end of August. So, the hope that prices were starting to settle back down is not so true. The Fed has plenty of firefighting yet to do.

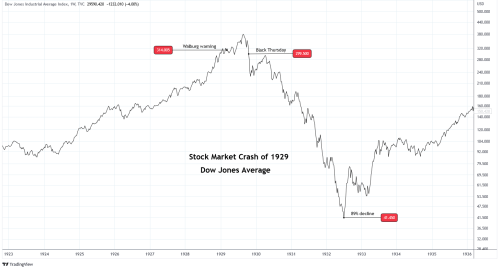

Stocks have a lot further to sink

As I showed in the last article, the blowout of the stock market, if it follows historical patterns for major crashes is exactly where one would expect it to be at this point in the cycle if it is merely halfway down to its ultimate resting place, which is with whale dung on the bottom of the sea.

The ship is sinking, and fear is rising, but it still hasn’t hit the all-out panic levels we’ve seen in other major crashes. Remember that when it does, the Dow has been known to fall as much as 1,000-3,000 points in a day during that phase, so the sea floor can rush up pretty quickly to meet us as the ship slides off the rocks. Don’t listen to those who say the market puts in a bottom when fear hits a high because, while that’s true, it only takes a few days for the Dow to be down another 5,000 points before the panic burns out. The fear doesn’t have to last long when you get to the scream leg of the journey.

As you can see, major stock crashes can play out for a very long time from their first precipitous declines before they take their worst decent to find the bottom. That’s the scream ride into the trench, and we haven’t even started screaming yet, though I think we’re close:

By “major,” I mean the kind of crash where everything breaks … like the Everything Bubble that is clearly breaking now.

Even when the stock market bounces off the bumpy bottom, the economy, which many forget is far from the same thing as the market, can keep sinking for months to come, leaving stocks to scrape without hope along that bottom as they did in the Great Depression for a year, rise a little more and then scrape along a couple more years because sentiment, after such a fall, can take a long time to rebuild. It took a quarter of a century for the stock market to fully recover its losses from the Great Depression.

If the NASDAQ, in the following graph, breaks its 200-week-average line of longterm foundational support that has held for years, it could be a disaster. Look at how long it has been since it did break that line and what happened back when it did:

Oops, it just did:

It was resting right on its 200-week moving average Thursday where support held up even in the crash of 2020, but then it punched through on Friday, as I started writing this article. Is this going to be a one-day test, or does the bottom now fall out because its most longterm trend line of support has failed?

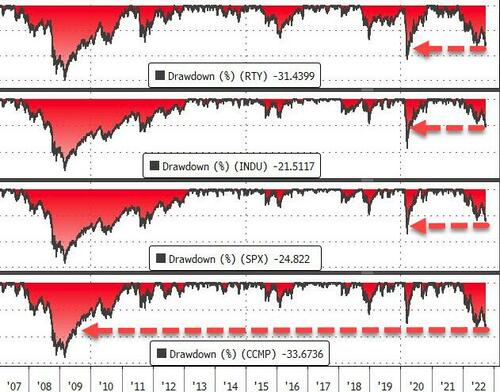

The only two times global markets have looked this bad in the past decade or so were in 2020 and 2008:

It’s the Everything Bubble

When the economy is reported as having gone down further in GDP for yet another quarter and everyone wakes up to realize we don’t have a strong labor market, we have a diseased labor market that only runs tight on labor because labor supply is so short because labor died or is literally (and perhaps permanently) sick, then we’ll know production is not going to readily rise anytime soon because there aren’t enough people to make things, and bonds may still have further to fall. (You can read the labor article referenced near the top of this post if you don’t understand what I’m talking about.)

I believe and have been saying all year, the bond market is going to bust into pieces all over the world and take major banks and many other big players like entire corporations out with it and will be worse than the stock-market crash. So far, that is the trajectory we are seeing. With many big funds down about 15% for the year, we’re not far from when the liquidations begin. Given where the US bond market is as we start October, the next Lehman moment may easily be an October surprise that sucks everything down steeper and faster in its undertow.

Globally, the bond market is in the worst shape we’ve ever seen. It’s already experienced the biggest drawdown in history due to the absurd central-bank boost it was given during the Coronacrisis, which central banks are now trying to unwind (the BOE with no success whatsoever):

BofA notes, regarding US Treasuries,

Thin UST liquidity & limited demand may make the US market vulnerable to a market functioning breakdown, similar to UK…. Fed could follow BoE in event of extreme UST market functioning breakdown.

And the UK blowout took about a day to suddenly emerge in front of us as the monster that was shadowing us just beneath the surface. So …

Spiraling losses on Wall Street are now snowballing into forced asset liquidation, according to Bank of America Corp. strategists.

The NYSE Composite Index, which includes US stocks, depositary receipts and real estate investment trusts, has broken multiple technical support levels including its 200-week moving average, the 14,000 mark, as well as 2018 and 2020 highs. Now accumulated losses could be forcing funds to sell more assets to raise cash, accelerating the selloff, according to Bank of America.

The “best Wall Street barometer” is breaking down, strategists led by Michael Hartnett wrote in a note on Thursday, keeping a tactically bearish view until panic selling forces a central bank intervention.

So, the crash of stocks could force people who have leveraged positions to liquidate their bonds to raise cash, while the crash of bonds may be forcing others to liquidate stocks. It’s all on fire. It’s getting dire out there. As ZH summarized its favorite quant on Friday …

The velocity of “things breaking” around the world (Yen, Yuan, Euro, Sterling, SONIA, Gilts, MBS, Lev Loan deals, the entirety of the UK LDI / Pension complex) is obviously a “neon swan” telling us that we are clearly now in the “market accident” stage from the tightening surge.

Moreover, …

As Larry Summers alluded on Thursday, when you mix extraordinary volatility with leverage and policy uncertainty, high underlying inflation and commodity uncertainty stemming from a war, firefighters shouldn’t take too many vacations.

That’s the situation report. Banks are concerned that the Fed is going to tighten us into a recession. Wait until they figure out we’re already more than three quarters into one, and the Fed’s still tightening, and inflation is still rising! Watch the waters boil then! But they won’t recognize that until they understand what has been communicated to you here already — that the tight labor market is no sign this time of a resilient economy. It is the exact opposite, which is why it is beguiling central banksters. Our financial leaders cannot wrap their heads around that because it is so engrained in their thinking to see it in the opposite way. It’s a blind spot as dark as a black hole, hiding the very light they need to see by.

In fact, even if you look at one of those areas that is supposed to stay subdued because it is the pool of money the largest institutions in the world use to hedge their bets, you find that interest-rate swaps have suddenly gone berserk, too:

Both were the largest one-day moves in either direction on record for the index, which was rolled out in October 2020.

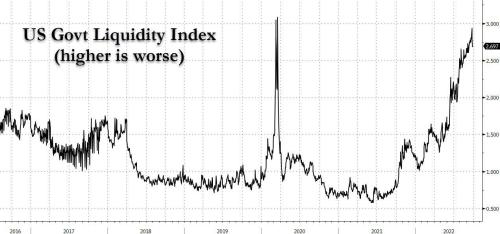

Those kinds of moves in relatively stable pools are dangerous signs that liquidity is tightening up, and, when liquidity gets thins, markets get brittle and snap. Yet, it is precisely right at this time that the Fed has doubled down on sucking money out of its foundational support for money supply (its balance sheet) to a rate that is now faster than at any time in history.

In fact, liquidity tightness in government instruments has only looked this bad during the most perilous financial times in history, so let’s double the tightening rate right now because, yeah, that seems safe:

OK, so that’s ugly, but it is also happening during a situation that hasn’t happened since 1929:

Through a series of prodigiously coincidental events, something is happening that has not occurred in over a hundred years: The Federal Reserve System of the United States is tightening monetary policy into a recession following an extraordinary period of financial speculation.

We are now sliding into the Marianas Trench of recessions

One commenter on my last article, where I said we’re crashing into a burning ring of fire, exclaimed,

Recession? Really, we have been in a recession and are now heading towards a depression.

I responded that is exactly where I’m going with this. Since the Fed is pounding us deeper when we’ve already been sinking for nine months because the Fed is too near-sighted (or drunk on the sherry it’s serving to all the passengers) to even recognize we’re already on the rocks, we are just starting to slide into a recession that I believe will be as bad as the recession referred to as “the Great Depression” — the Marianas Trench of recessions.

Another asked when does it move from being a “recession” to a “depression,” and my response was that it IS moving there now, but that “depression” has no economic definition that everyone more or less agrees on. So, yes, I fully believe we are sliding into a time that will be in its own ways as perilous as the Great Depression, and I wouldn’t be surprised if we eventually call it “The Second Great Depression” (like the Second World War) or, in modern terms, “The Great Depression 2.0.” (For my full response on the difference between a “depression” and “recession” and why I called this The Great Recession Blog in the first place because of where I believed we were headed, click here.)

The situation described in the above section is far from a stable set of circumstances in which to be doubling down on how hard you are tighting, so I fully expect things to get seriously worse, and fast. In the UK, it IS worse as pension funds are now scrambling all over the place to make their margin calls.

“There’s a lot of pain out there, a lot of forced selling,” said Ariel Bezalel, fund manager at Jupiter. “People who are getting margin called are having to sell what they can rather than what they would like to.”

“There could be many hundreds of schemes that have had their hedges reduced or removed. This means their funding positions are now much more vulnerable than they were a week ago.”

But this isn’t going to restrict itself to the UK. Everything is intertwined, and everything is breaking up: Supply chains are broken into individual shattered links all over the world. Food shortages are appearing all over the world and are certain to get much worse this winter. The world is at war. We have an energy crisis equal in severity to the one in the 70’s recession, maybe worse. The labor force is literally decimated by disease or vaccines (as in reduced in size by 10%). Bonds are crashing hard, as shown above. Stocks are clearly crashing hard, as no one can deny, and there is good reason to believe they have a good distance to fall in order to get back on track with our rapidly falling economic reality and with their own remaining support levels. Housing is falling quickly. Banks are starting to warn of serious trouble, and the defaults have hardly begun; yet, central banks are rapidly withdrawing their support of money supply at a time when we have already been in a recession for nine months, but which we remain in total denial of, so we keep making it worse; while inflation is burning the banksters backsides up, so they don’t have much choice but to keep fighting the inferno, exactly the jam between a rock and a hard place I said almost two years ago they were heading themselves into. Meanwhile, droughts and simultaneous floods are making the shortages worse. Social divisions are more strident than they have been since Vietnam. We are less cohesive as societies than we were in Great Depression so in less of a good position to weather through together.

You can call that a “depression,” and I’ll agree, but I gave it another name of its own when I started talking about it coming a few years ago. I called it “The Epocalypse,” which I defined as being an economic apocalypse that would be truly epic in scale and would become known as its own small epoch in time.

Tick, tock, the Lehman moment is getting closer somewhere in the world … and October does love a surprise! In fact, taking all markets in the US into consideration — stocks, bonds, housing, precious metals, cryptos — more money has already been lost this year than during the entire Great Recession! And we haven’t even had our big moment yet! It just keeps coming!

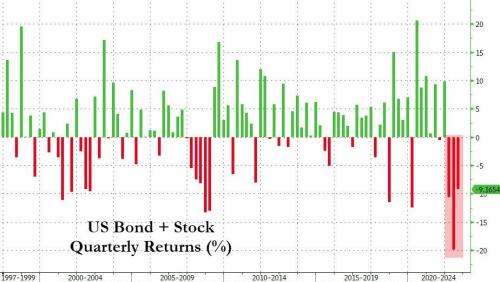

In all, this year has been, in very fact, the worst period ever for balanced stock-and-bond portfolios:

The phantom Powell pivot

In spite of all these obvious economic troubles, we just had a big bear-market rally in which many fools fantasized stock troubles were actually over because everyone everywhere (even Zero Hedge) kept whipping up the fantasy that the Fed would soon pivot! However, ZH, at least, is now off the pivot bandwagon:

We note that US financial conditions have tightened dramatically in the last quarter as Powell punched the ‘pivot-hopers’ in the face…

So, let’s hope that kind of denial is finally behind us and clear heads prevail. Those tight US financial conditions now look like this:

Bear-market rallies always form around some kind of hallucinogen, and the “Powell pivot” was the opiate of choice for this last sucker’s rally.

The bear-market rally happened because markets – meaning folks and algos playing in them – had this fabulous reaction to the Fed’s aggressive rate-hike scenario: They began fantasizing about a Fed “pivot” and about rate cuts and some even about QE all over again. Asset prices began to jump and yields began to fall.

I felt like a pretty lone voice beating the drum to say a Powell pivot was never going to happen, especially when even ZH was saying the opposite, but that’s because so few people understand the true nature of our crippled job market. It was frustrating to say the least … and thankless even when Captain Powell proved he wasn’t about to pivot. Suddenly, people started talking like they knew that all the time, but I never heard any of them saying it!

When the job market is tight because so many in the labor force died and so many more are off with longterm chronic illness (5-million in all according to the Brookings Institute; again, see the key article referenced above if you’re not familiar with this yet), then you have to eliminate an awful lot of jobs before you get jobs back down to where they merely match up with the available labor force, much less to where you will see unemployment claims start to rise. We have far more jobs than labor, not because jobs are back to trend, but because labor supply is far below trend and will remain there. It’s going to be a shocking reality check for the Fed and its followers if they ever get their heads clear on the labor situation.

The fall from a bear-market rally is a rough one as Wolf Richter notes:

Many of us in our illustrious comments on Wolf Street had been expecting a rally. And I drew parallels to the bear-market rally during the dotcom bust. During that rally, which lasted less than two months, from May 27 through July 17, 2000, the Nasdaq jumped by 33% without ever getting back to its old high. Ultimately, the Nasdaq collapsed by 78%.

That bear-market rally in the summer of 2000 suckered a lot of people back into the market, thinking that stocks would be going to the moon again, and they got crushed.

The 2022 bear-market rally started in mid-June and also lasted two months. It came as the Fed-pivot-fantasy mongers – including some well-known hedge-fund managers – had fanned out across the financial media, the social media, and the rest of the internet, asserting that the Fed would soon pivot, that in fact it wasn’t even doing QT after all, and yada-yada-yada.

So we got a huge two-month rally, and the Fed-pivot mongers, including the hedge funds, that got out in time made a huge amount of money. But those people that believed the pivot fantasy and bought when the pivot-mongers sold, well, those folks took the losses. But that’s how it always goes.

However, there is one key difference between now and the dot-com bust that makes now much more dangerous. In past times, when the Fed did make a pivot, and this was one of the keys I presented for understanding why a pivot would not happen this time,

inflation was at or below the Fed’s target, and the Fed was just trying to “normalize” policy, and it was just trying to bring its balance sheet down to a manageable level. It just wanted to get back to some kind of “neutral.”

The Fed, in other words, wasn’t trying to fight inflation at all. It was merely trying to normalize its balance sheet. It had zero pressure to keep tightening. That left it completely free to rush right back in with more QE if the markets started to rebel to the tightening, which they did.

Nevertheless, Powell came under withering pressure from Trump, who’d taken ownership of the Dow. And with inflation below the Fed’s target, and with the Dow in free-fall, and with Trump keelhauling Powell on a daily basis, the Fed did its infamous pivot, and markets soared again.

With almost zero inflation, the Fed had ample room to pivot and, in fact, good reason to return to easing just to get inflation up to its target. Now it has NONE — NO ROOM WHATSOEVER. It’s sink the economy or burn it up in a great inflation inferno, and who knows whether it is worse to die by fire or ice.

The lesson was this: These artificially inflated markets cannot even maintain their level amid rate hikes and QT. Even little-bitty rate hikes, just four in a year, and small amounts of QT caused markets to tank, just like interest rate repression and QE had caused them to soar. It was becoming clear to everyone: QT was having the opposite effect of QE.

YES. And, so, what are markets going to do now when the Fed cannot return to the easing game without throwing gasoline on the inflationary ring of fire that surrounds all of us and them, so it is fighting inflation faster than it ever has? One other difference? Last time the economy was not sinking deeper and deeper into recession as it is now.

There is no “soft landing” when you’re already on the rocks but are too near-sighted to even recognize it, in spite of two solid quarters of declining GDP already recorded. It’s as if the Fed is dropping the plumb line, which is immediately pinging off solid rock, but the Fed is still saying, “Plenty of fathoms here!”

So, as Wolf summarizes,

In 2022, inflation has spiked above 8%, highest in 40 years, and has spread across the economy and is now spiking in services, away from supply chains and commodities, even as some goods inflation has started to unwind. And there isn’t going to be a Fed-pivot until this inflation is making “compelling” progress, as the Fed calls it, in heading back to 2%, which could be a long way off.

Now some are arguing the Fed will pivot when something breaks, but what does that matter? Whatever breaks in the present circumstances of financial disasters piling up all over the world is going to cascade into other things and reverberate throughout the world of troubles to where a Fed return to QE will be meaningless. It’s like saying, the Fed will hoist the sails again as soon as the pieces of ship slide off the rocks. Who cares? It’s irrelevant at that point because, by then, we’re already as good as sunk.

So, grab the flotsam and forget the Fed!

The biggest thing that the Fed is in charge of has already broken: price stability. Inflation is the worst it has been in 40 years. And the Fed is tightening in order to fix this huge thing that has broken – to bring this inflation back under control and down to 2% (as per core PCE). This could be a long and tough slog.

As Mohamed El-Erian just noted,

This pivot only happens if you have an economic accident or a financial accident. And the journey to an economic accident or a financial accident is a very painful journey.

So, forget the pivot. It will be completely meaningless by the time the Fed does return to QE.

It’s in its prime directive of price stability that the Fed has clearly already lost control. Once the Everything Bubble has broken across all of the oceans of the world, the Fed can go back to QE all it wants, but that’s not going to end severe supply shortages; its not going to make a dead and languishing labor market return to health; its not going to restore peaceful and functioning borders for trade; and, it’s questionable QE will even be able to fix the things it is supposed to be able to fix, such as busted banks, because it’s questionable anyone will even be willing to believe in it anymore because the Fed is losing the one thing it can least afford to lose — credibility.

The Fed, itself, may not survive the blame it will receive. In fact, we can only hope it doesn’t!

In conclusion … real, final conclusion perhaps

This blog may not survive either. I’ve been a strident voice and sometimes boastful sounding because I’ve been trying desperately for years to gain attention to this message and to get people to believe in this message and to recognize that where we are headed is predictable. That’s not how I am in person, but I have been trying hard to pound the message here, especially in the last few years, because it has not been gaining traction or getting attention. If you lack credentials in the field, no one cares what you have to say because they pay far more attention to credentials than to thoughts. So, I beat the drum hard.

It hardly helped. This blog continues to have exactly the same average number of readers each month as it had many years ago. It never rises to continue floating higher. Some come and love it for awhile and then go away, perhaps because of the boasting, which is to try to get people to see these things can be seen as to where they are headed, or perhaps it is because of my sometimes strident tone due to the urgency I’ve felt behind the message or the frustration I feel with the endless denial and the Fed’s endless stupidity. I’ve lost the patience to call it anything other than that. (Though I can go along with “just plain evil.”)

After all these years, the blog still averages about 300 readers a day when I don’t publish an article, exactly the level it cruised along at by the end of its first year, and about 2,000-5,000 on a typical good day when I publish one of my own articles and other sites pick it up and refer to it — also the same as way back then. As you can see, those articles are often complex, trying to take in a lot of news and bring it together and then distill it into some sort of meaning, so I can’t knock out one a day. It takes time just to collect the stories that typify the week and determine the trend, and by then there is a lot to say and a long article to edit. It’s not sound bytes.

At the same time, The Daily Doom hasn’t taken off either. It’s gained about forty people (net) since I started putting it together — about one a day. I was hoping it might, by good fortune, go viral if put on a different venue. Likewise the attrition rate in Patreon support has always been almost equal to the new support, so that has remained barely growing for years at a level that still comes to about $5 an hour for my time (though I am truly thankful to those who have joined in that support and especially those who have stayed with me for some time to say my time is worth something to them; they are my driving force). Even comments have fallen off as regular readers and commenters moved on.

I’m not sad about it. It just is what it is, but I’m at a juncture in life where I am giving serious time to evaluating whether to continue with either The Great Recession Blog or the The Daily Doom, the latter having been just an experiment anyway because one reader suggested I try doing something on Substack, and that seemed interesting and well-suited to me, and plowing through a lot of news is something I do daily for this blog anyway. If support or readership were to suddenly leap forward, I would continue with either one; but I’m thinking it may be time to move on to things that I find simply more fun or creative or spiritually invigorating or … not sure. Just thinking. If not in one of those directions, then certainly to something that pays better.

I’ve asked for comments about the blog and about The Daily Doom, but have heard from only a couple of people. I’m fine with hearing negative feedback, as I’d rather know than not know. So, if you are someone who was a regular reader and have stopped being one but just happened by, I’d be interested in hearing why you stopped being regular. I’m interesting in hearing the ideas of anyone, but mostly it is just a matter of either financial support or readership or both taking a big leap forward because, if I can’t make that grow on a blog like this in times like this, then what am I even doing?

Reprinted with author’s permission from The Great Recession Blog

The shortcode is missing a valid Donation Form ID attribute.